Indonesia’s digital economy has come a long way in the last decade. In the previous decade, due to the limited payment infrastructure, bank transfers were often the only option provided to consumers for making purchases. However, the selection of payment methods has progressed by leaps and bounds since then. One of the payment methods available today is Direct Debit.

How does Direct Debit work?

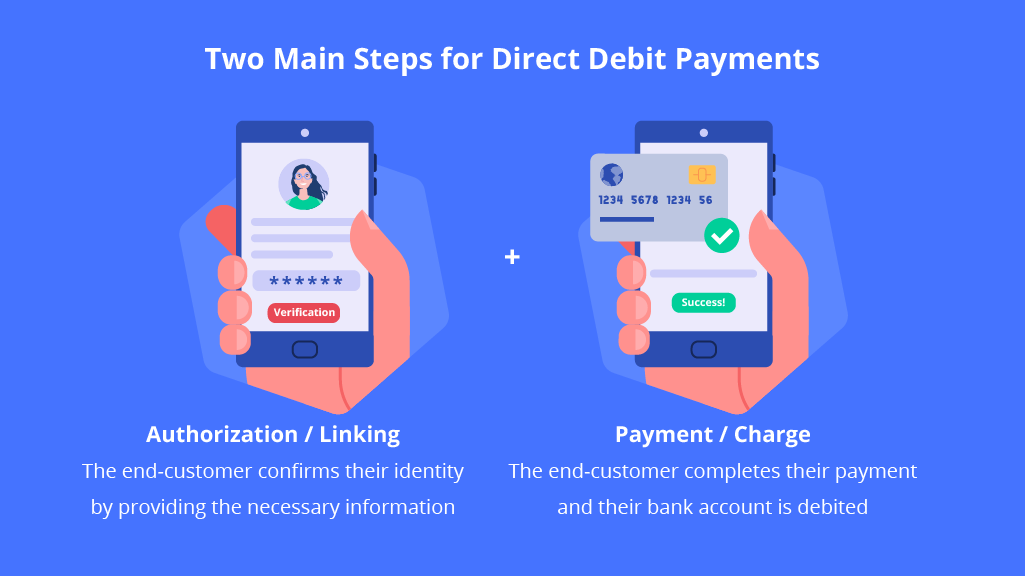

Direct Debit is a payment method where end users can register their debit cards or online bank login with a merchant or marketplace to pay for their purchases. After a one-time authorization, merchants can pull funds directly from an end user’s bank account.

Speed and automation are one of the main reasons for the development of payment methods in Indonesia. This is consistent with our internal data, which shows the top payment methods to be those that help speed up the payment process, such as virtual account, e-Wallet, QR Code, and Direct Debit.

Why choose Direct Debit?

With e-commerce and online transactions, cart abandonment or payment drop-off rates can be close to 70%, according to the Baymard Institute. This makes it crucial for businesses to address and reduce friction to improve their customer checkout experience and increase revenue.

Direct Debit is a game changer for merchants. With Direct Debit, you can provide seamless payment flows for your customers, reducing payment drop-off rates and allowing you to settle payments instantly.

Benefits of transacting with Direct Debit

Direct Debit is important for reducing cart abandonment because it addresses many reasons why buyers abandon their carts. Here are a few ways Direct Debit solves the common causes of abandoned carts:.

- No more unnecessary check-out steps

The more steps there are in a payment flow, the more opportunities there are for end customers to hesitate in completing the transaction. Direct Debit runs on tokenized payments, enabling merchants to enjoy a one-click payment flow. This significantly reduces payment friction. - No app hop-off

When using other payment methods such as virtual accounts, end customers have to either go to the ATM or move out of the checkout page onto their mBanking app. This app hop-off presents a chance for the customer to get distracted or to change their minds. On the other hand, Direct Debit offers a single-page flow. The customer won’t have to shift to a different app, so they’re more likely to complete their payment successfully. - Less chance of having an insufficient balance or credit

End customers do not always keep track of balance in their accounts and may have insufficient balance or credit. Hence, there is a higher probability of payment failing if the end customer uses eWallets or credit cards. Direct Debit is linked to the end customer’s bank account, resulting in a higher likelihood of a successful payment - Avoid per transaction authorization issues

Payment drop-offs often happen when end customers are not able to receive SMS, have forgotten their PIN or have mobile app issues. With a tokenized payment flow that comes with Direct Debit, end customers only have to authorize once. Merchants can avoid any authorization issues for subsequent transactions.

As an additional benefit, for banks in Indonesia, Direct Debit does not require compulsory OTP on each transaction. OTP on every transaction blocks merchants from supporting subscription models or payment plans. Xendit helps to solve this by offering Direct Debit without OTP and a recurring payment APIs for our merchants.

Currently, Xendit provides Direct Debit channels with BRI, Bank Mandiri, and BCA in Indonesia

Also read: Digital Business and the Potential of Young Entrepreneurs in Indonesia- Xendit Index 2022

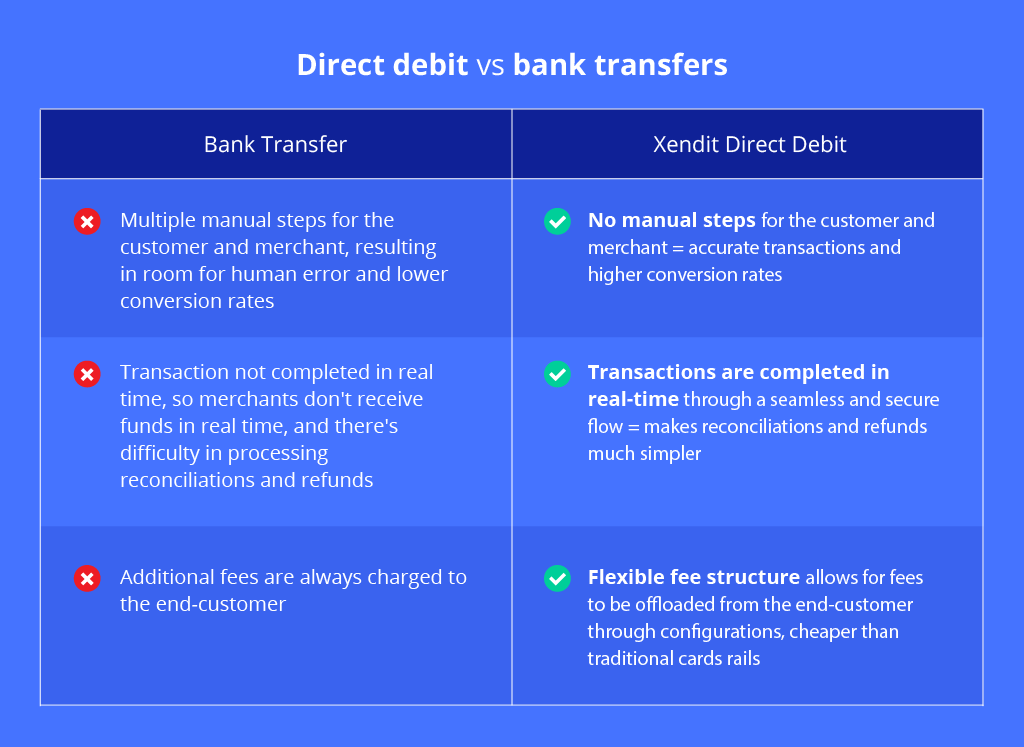

Direct Debit vs bank transfers

When evaluating their choices, merchants often compare Direct Debit with bank transfers. There are significant differences. Here are the highlights:

While funds are pulled from the same account, Direct Debit is not a regular bank transfer. With bank transfers, end customers would have to manually input the destination account as well as the amount that they want to transfer. This could result in human error, be it transferring to the wrong account or transferring the wrong amount.

On the other hand, Direct Debit pulls funds directly from end-customers’ online bank accounts. Unlike bank transfer, where customers would have to input the destination and amount manually, Direct Debit allows the amount to be entered and payment triggered by the merchant.

This tokenized payment flow enables one-click checkout for high ticket items, helping relieve inconvenience in the checkout process. On top of that, merchants can enjoy instant settlement and fees significantly lower than traditional credit card fees.

Here are a few use cases where Direct Debit can be highly beneficial for merchants:

- E-commerce business – Increase payment acceptance rates for high-value items with Direct Debit and receive payments with fast settlement times

- Subscription services – Auto debit (recurring) from your user’s bank account without the need for authentication each time. Some examples include collection of membership fees, SaaS services, Over-the-top (OTT) media services

- e-Wallet top-ups – Move funds from the user’s bank account to your e-wallet easily and quickly without performing multiple tedious steps

- Financial services – Secure payment infrastructure that enables financial companies to receive high-value payments on a recurring basis – insurance (annual/ monthly), investment plans

Also read: A guide to Indonesia eCommerce market

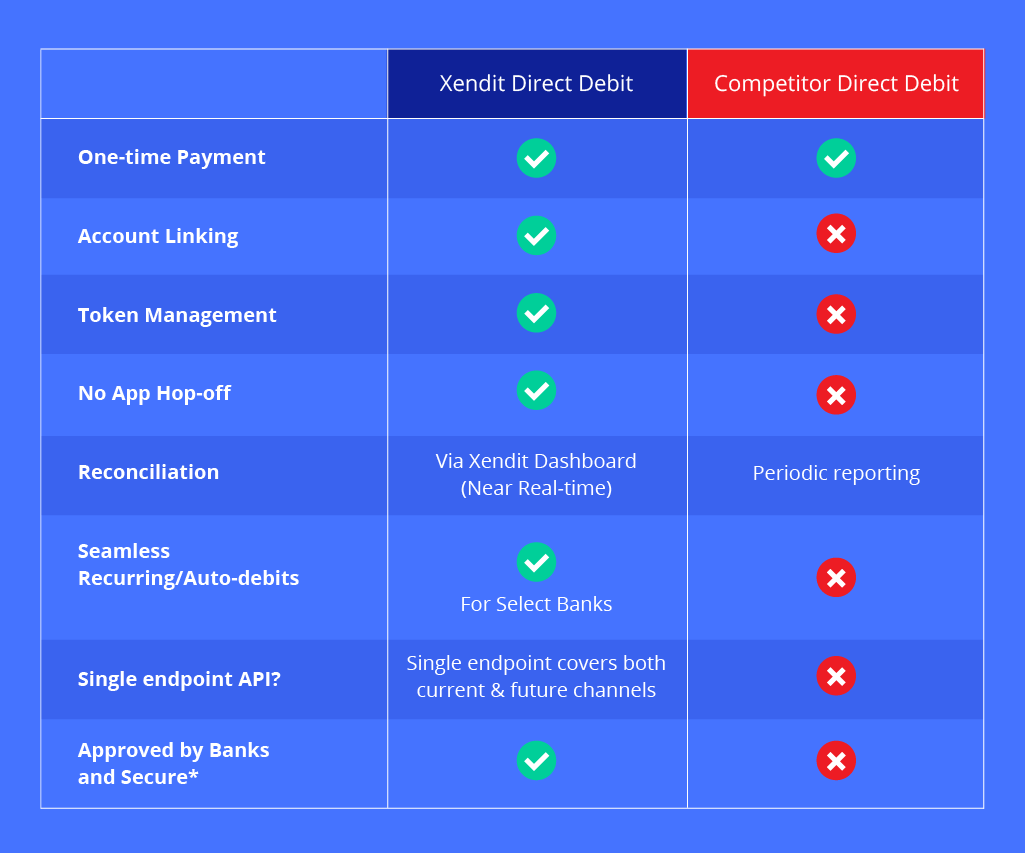

What makes Xendit’s Direct Debit different from others?

* risk of banks turning off connections due to unsecure indirect integrations

One key difference between Xendit’s Direct Debit offering and other competitors’ is that competitors often only offer one-time payment capability. But as discussed earlier, businesses stand to benefit from being able to pull funds on a recurring basis without tedious authorization each time.

Xendit offers the ability to link customer accounts and perform seamless recurring auto-debits. Businesses can also reconcile their transactions directly in Xendit dashboard in near real-time, as opposed to periodic reporting others usually provide.

On top of that, our customer support team is always ready to help–with 24/7 live agent chat and email support in Indonesia.

Sign up now and start boosting your revenue with Direct Debit!

About Xendit

Xendit is a financial technology company that provides payment solutions and simplifies the payment process for business in Indonesia, the Philippines, and Southeast Asia, drom SMEs and e-commerce startups to large enterprises. Amidst the fragmented payment landscape in Southeast Asia, Xendit enables businesses to accept payment from Direct Debit, virtual accounts, credit and debit card, eWallets, retail outlets, and online installments.

For many businesses, accepting payment online is new territory, but we’re here to help. We helped 1000s of businesses come online and we’d love to help you too.

Find out more about Xendit, or sign up to try our dashboard!