In the previous part of our risk management series, Risk management: What it is and its role in business success, we explored the basics about different types of risks and what roles risk management plays.

Now, in this second part, we want to equip you with the ability to take concrete actions to manage your business risks better. We’ll explain the foundational elements of a risk management plan, complete with actionable steps and real-world examples to help you understand better. Towards the end, we will share an example of a comprehensive and practical risk management plan that you can adapt for your business.

Let’s get started.

Fundamentals of a risk management plan

To effectively manage risks within your business, it is essential to develop a comprehensive risk management plan. This plan should outline the specific steps and strategies you will take to identify, assess, and mitigate risks. Here are some key components to consider when developing your risk management plan:

1. Identify risks

Conduct a thorough analysis of your business operations and identify potential risks. This can be done by performing risk assessments, engaging in discussions with employees, consulting with industry experts, and analyzing historical data. Risks could span operational, financial, reputational, compliance, and strategic domains. For instance, a restaurant business might identify supply chain disruptions due to food sourcing as a significant operational risk.

2. Assess risks

Evaluate the likelihood and potential impact of identified risks. This will help prioritize risks and allocate resources for their mitigation. Use a risk matrix or scoring system to quantify risks and determine their significance. For example, a software company might evaluate the risk of data breaches as high due to the sensitive nature of customer information.

3. Implement controls

Develop and implement appropriate controls and measures to mitigate identified risks. This can include implementing safety protocols, enhancing cybersecurity measures, training employees on risk management practices, or establishing contingency plans. For example, an e-commerce platform might implement robust cybersecurity measures and data encryption to mitigate the risk of cyberattacks.

4. Monitor and review

Continuously monitor and review the effectiveness of your risk mitigation strategies. Regularly assess changes in risk profiles, evaluate the effectiveness of controls, and make necessary adjustments as required. The business landscape is dynamic, and new risks can emerge while existing ones may evolve. Stay agile and adapt your strategies accordingly.

5. Communicate and train

Establish effective communication channels to share risk information with relevant stakeholders. This includes providing training and guidance on risk management practices to employees, creating awareness of risk management within the organization, and promoting a risk-aware culture.

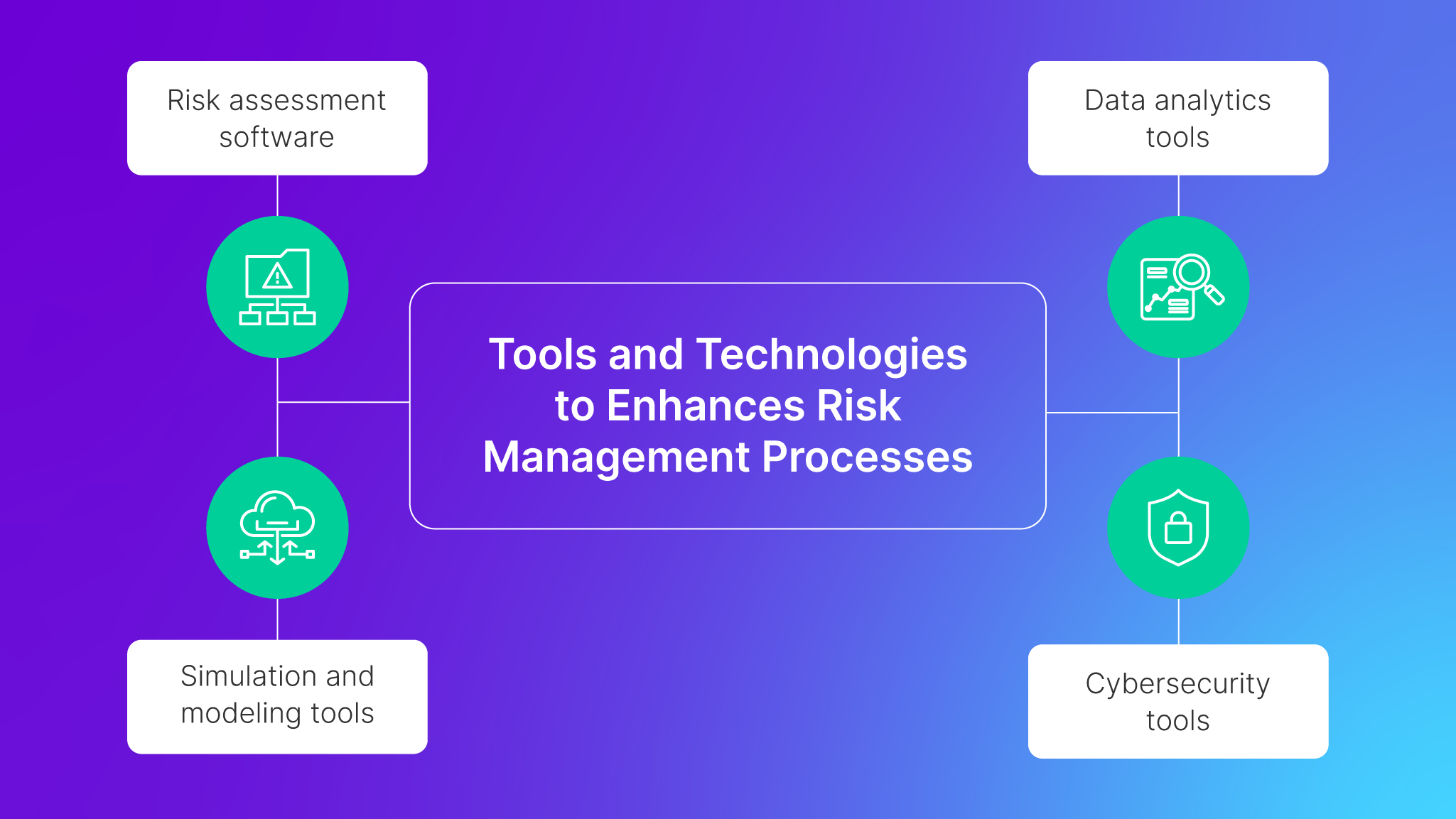

Tools and technologies to enhance risk management processes

Advancements in technology have revolutionized risk management processes, providing businesses with powerful tools to identify, assess, and manage risks. Here are some tools and technologies that can enhance your risk management processes:

- Risk assessment software: Risk assessment software automates the process of identifying and assessing risks. It allows you to centralize risk data, analyze risks using predefined criteria, and generate reports. This can save time and improve the accuracy of your risk assessments.

- Data analytics tools: Data analytics tools can help you identify patterns and trends in your data, enabling you to make more informed decisions. By analyzing historical data, you can identify potential risks and predict future outcomes.

- Simulation and modeling tools: Simulation and modeling tools allow you to simulate various scenarios and assess their potential impact on your business. This can help you evaluate the effectiveness of different risk management strategies and make data-driven decisions.

- Cybersecurity tools: To mitigate cybersecurity risks, businesses can utilize a range of cybersecurity tools, such as firewalls, intrusion detection systems, and encryption software. These tools can help protect your data and systems from unauthorized access and cyber threats.

By leveraging these tools and technologies, you can streamline your risk management processes, improve decision-making, and enhance the overall effectiveness of your risk management strategy.

Sample risk management plan for a medium-sized F&B company in Indonesia

Knowing concepts and textbook knowledge is different from applying them to real-life situations. Thus, we have crafted a sample risk management plan that is both practical and comprehensive to help you get started! This plan is based on a medium-sized food and beverages (F&B) company based in Indonesia. You can use this plan as a guide and adapt it according to the nature of your business and business needs.

Step 1: Risk identification

1.1. Establish a cross-functional team: Assemble a team comprising representatives from various departments including operations, supply chain, finance, marketing, and legal. Their diverse perspectives will ensure that you are identifying risks comprehensively from several different angles and help minimize blind spots.

1.2. Brainstorm potential risks: Conduct brainstorming sessions to identify risks specific to the F&B industry in Indonesia, making sure that you consider both internal and external factors. Examples include supply chain disruptions, food safety concerns, regulatory changes, market competition, and reputational issues.

Step 2: Risk assessment

2.1. Quantify impact and likelihood: Use a risk assessment matrix to rank risks based on their potential impact and likelihood of occurrence. Assign scores to each risk to prioritize them effectively.

2.2. Scenario analysis: Develop scenarios for the top-priority risks to understand their potential consequences. For instance, analyze the effects of supply chain disruptions on production and customer demand.

Step 3: Risk mitigation strategies

3.1. Develop mitigation plans: For each high-priority risk, formulate clear mitigation strategies. These strategies could involve process improvements, resource allocation, alternative suppliers, and diversification of products.

For example:

- Supplier relationships: Establish strong relationships with local suppliers and consider sourcing from multiple suppliers to reduce the risk of disruptions.

- Food safety protocols: Implement stringent food safety protocols to prevent contamination and ensure compliance with local regulations.

Step 4: Contingency planning

4.1. Create contingency plans: Develop contingency plans outlining specific actions to take if a risk event occurs. Include responsibilities, communication channels, and necessary resources.

4.2. Emergency response: Establish procedures for handling emergencies such as product recalls or foodborne illness outbreaks. Ensure employees are trained in executing these procedures.

Step 5: Risk monitoring and review

5.1. Regular monitoring: Assign responsibility for monitoring and reviewing identified risks regularly. Utilize key performance indicators (KPIs) to track the effectiveness of mitigation strategies.

5.2. Adaptation: Stay agile and adapt your risk management strategies as circumstances change. If new risks emerge or existing ones evolve, update your plans accordingly.

Step 6: Communication and training

6.1. Internal communication: Ensure all employees are aware of the identified risks, mitigation strategies, and contingency plans. Regularly communicate updates and changes.

6.2. Training programs: Implement training programs to educate employees about risk awareness and the importance of adhering to protocols. This includes food safety training for staff in direct contact with food products.

Step 7: Regulatory compliance

7.1. Stay updated: Keep abreast of the latest regulations and guidelines in the F&B industry in Indonesia. Ensure your operations remain compliant with local laws related to food safety, labeling, and environmental regulations.

Step 8: Continuous improvement

8.1. Periodic review: Conduct periodic reviews of your risk management plan to assess its effectiveness. Identify areas of improvement and implement necessary changes.

8.2. Feedback loop: Encourage employees to provide feedback on potential risks they observe during their day-to-day tasks. This can enhance the accuracy of risk identification.

A resilient business is the first step to success

In the multifaceted business world, a well-structured risk management plan serves as your compass, helping you navigate challenges and seize opportunities. By identifying, assessing, and addressing risks systematically, you’re not just protecting your business—you’re advancing it towards robust growth.

We hope that you are now well-equipped and ready to take on risk management for your business! Do check out our Part 1 of our series—Risk management: What is it & its role in business success—if you haven’t.

Next, in the third and last part of our risk management series, we will delve into the topic of Enterprise Risk Management (ERM) and the difference between that and traditional risk management. Keep a lookout for part 3 of the series!