With e-commerce and online transactions, cart abandonment or payment drop-off rates can be up to 70%. This makes it crucial for businesses to address and reduce friction to improve their customer checkout experience and increase revenue.

Xendit’s Direct Debit product is the game-changer for our merchants. With our direct debit, merchants can provide seamless payment flows for their customers, reducing drop-off rates from customers. Xendit provides direct debit channels with two of the biggest banks in the Philippines, UnionBank and BPI.

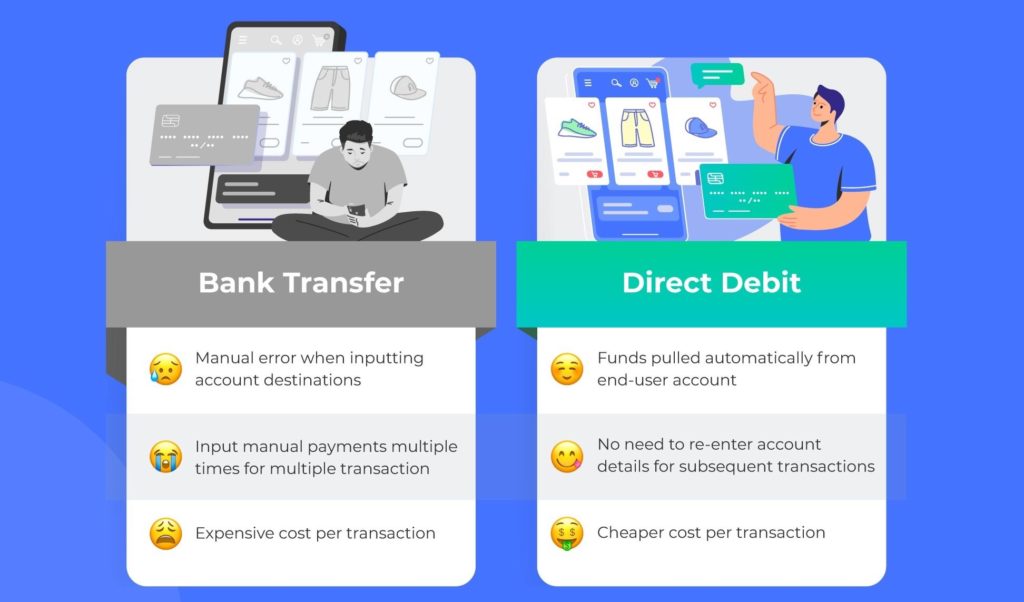

Direct Debit vs Bank Transfers

While funds are pulled from the same account, direct debit is not a regular bank transfer. With bank transfers, end-customers would have to manually input the destination account as well as the amount that they want to transfer. This could result in human error, be it transferring to the wrong account or the wrong amount.

On the other hand, direct debit pulls funds directly from end-customers online bank accounts. Unlike bank transfer where customers would have to input the destination and amount manually, direct debit allows the amount to be entered and payment triggered by the merchant. This tokenized payment flow enables one click check-out for high ticket items, helping relieve inconvenience in the checkout process.

Direct Debit can help solve the following key reasons why users drop-off.

- Unnecessary check-out steps – the more steps there are in a payment flow, the more opportunities for end customers to hesitate in completing the transaction. Direct debit runs on tokenized payments, enabling merchants to enjoy one click payment flow. This significantly reduces payment friction.

- Insufficient balance or credit – end customers do not always keep track of balance in their accounts, there is a higher probability of payment failing if the end customer uses eWallets or Credit Cards. Direct debit is linked to the end customer’s bank account, resulting in a higher likelihood of a successful payment

- Per transaction authentication issues – payment drop offs happen when end customers are not able to receive SMS, forgotten PIN or mobile app issues. With a tokenized payment flow in direct debit, end customers just have to authenticate once and avoid any authentication issues for subsequent transactions.

- Compulsory OTP requirement – OTP on every transaction blocks merchants from supporting subscription models or payment plans. Xendit helps to solve this by offering direct debit without OTP and a recurring payment APIs for our merchants

Direct Debit is ideal for

- Ecommerce business – Increase payments acceptance rates for high value items with direct debit and receive payments with fast settlement times

- Subscription services – Auto debit (recurring) from your user’s bank account without the need for authentication each time. Some examples include collection of membership fees, SaaS services, Over-the-top (OTT) media services

- Mobile Wallet top ups – Move funds from the user’s bank account to your e-wallet easily and quickly without performing multiple tedious steps

- Financial services – Secure payment infrastructure that enables financial companies to receive high-value payments on a recurring basis – insurance (annual/ monthly), investment plans

How does Xendit’s Direct Debit work?

When merchants enable direct debit payments via Xendit, end-customers can select direct debit payments on the merchant’s checkout page. End customers can then register their debit cards or online bank login. After a one-time authorization, merchants can pull funds directly from an end user’s bank account without OTP for subsequent payments.